“Despite some of the monthly pullback, it is important to note that sales remain exceptionally strong and are likely being limited due to supply choice in the market,” said CREB® Chief Economist Ann-Marie Lurie. “While further rate increases will likely start to dampen demand later this year, more pullbacks in new listings this month are ensuring the market continues to favour the seller, resulting in further price gains."

New listings trended down relative to last month and levels recorded last year. With the sales-to-new listings ratio remaining above 74 per cent, there was not much of a shift in overall inventory levels.

With 4,850 units in inventory, we are nowhere near record low inventory levels, however, levels are far lower than what was recorded in April since 2014. What has changed in the market is the composition of the inventory levels. When comparing inventories today to what was available in 2014, we can see that detached homes comprise of a smaller share of the inventory levels especially for properties priced below $500,000.

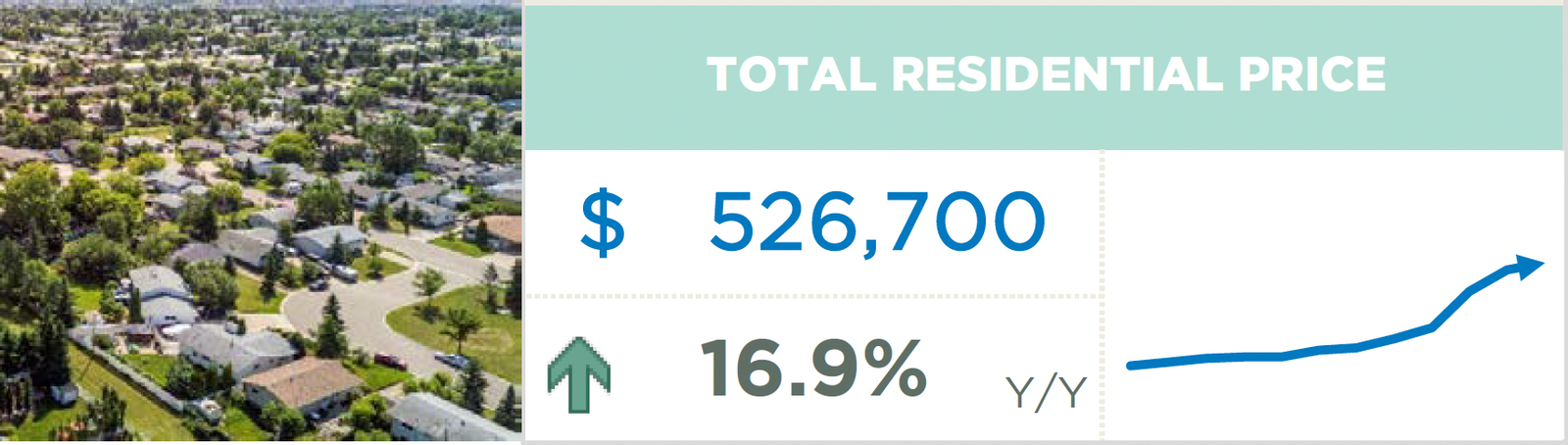

Overall, the Calgary market has seen the months of supply remain below two months since November of last year, placing significant upward pressure on prices. The benchmark price in April reached $526,700, which is nearly two per cent higher than last month and 17 per cent higher than last year.

Housing Market Facts

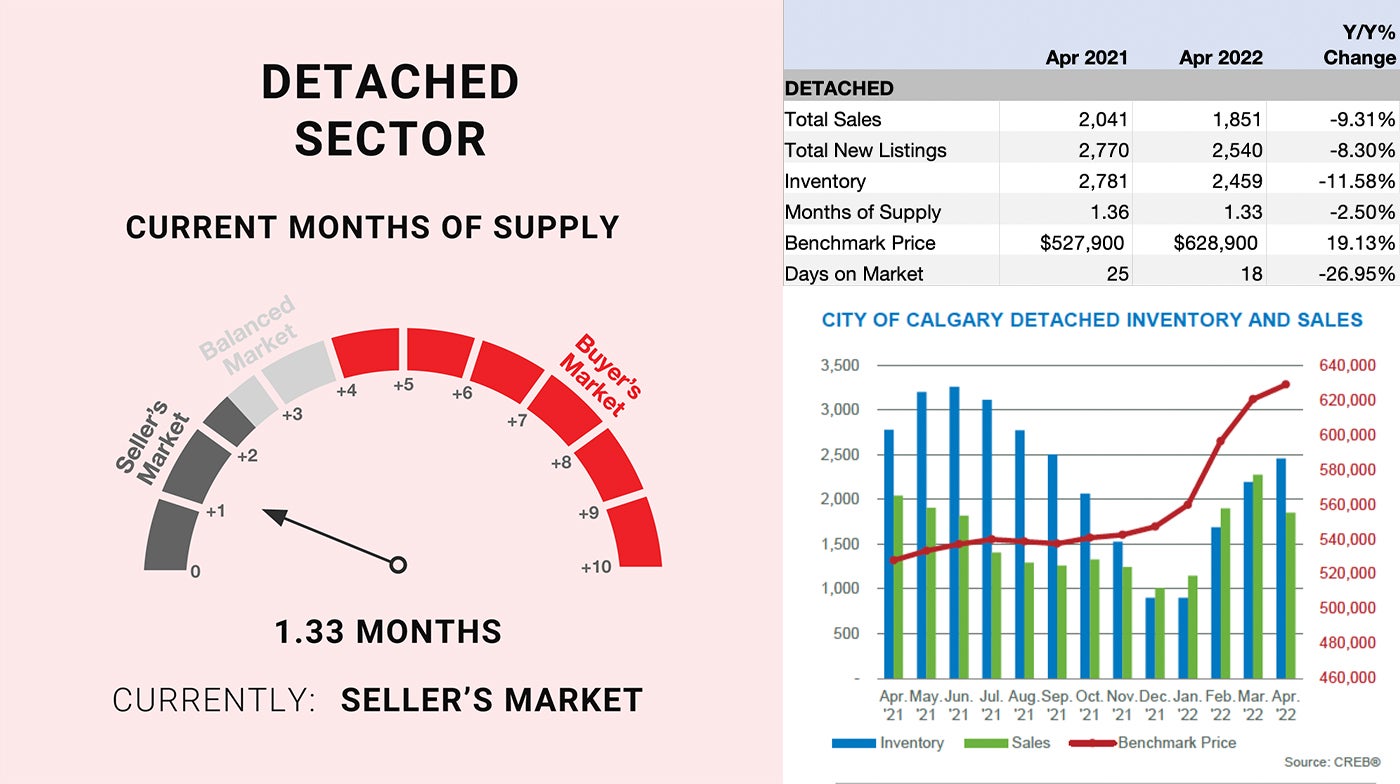

Detached

For the first time since spring of 2020, year-over-year sales slowed down. While sales have dropped, it is important to note that with 1,815 sales, this is still far stronger than long term trends. A decline in sales occurred for homes priced under $600,000. This pullback in sales for lower priced homes was likely related to further supply declines driven from reductions in new listings in those price ranges. Inventories in the detached sector have not been this low for the month of April in nearly 15 years.

While the slightly slower sales compared to inventory levels did help push the months of supply back above one month, conditions continue to remain exceptionally tight with 1.3 months of supply. This continues to place upward pressure on prices, but at a slower pace than the last three months. The detached benchmark price rose to $628,900 in April, which is 19 per cent higher than last year.

While the slightly slower sales compared to inventory levels did help push the months of supply back above one month, conditions continue to remain exceptionally tight with 1.3 months of supply. This continues to place upward pressure on prices, but at a slower pace than the last three months. The detached benchmark price rose to $628,900 in April, which is 19 per cent higher than last year.

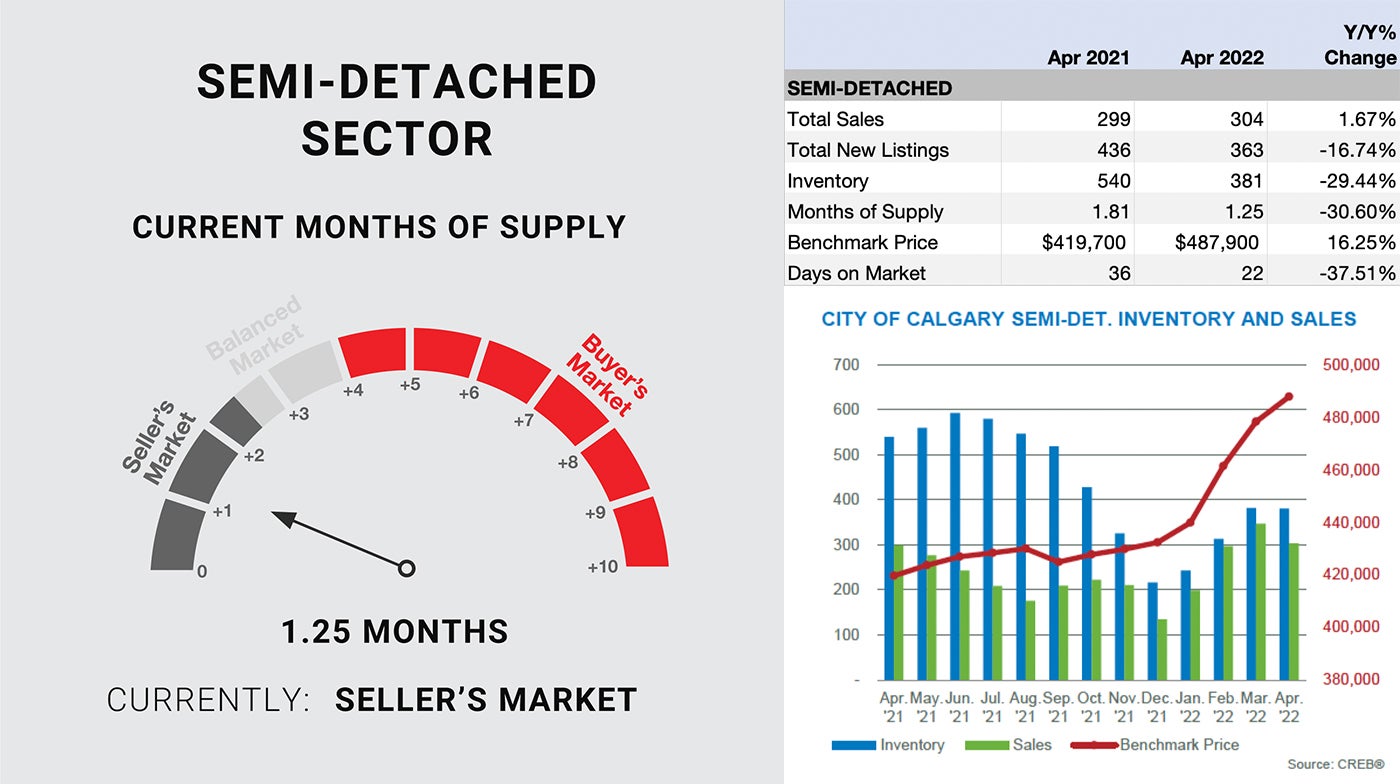

Semi-Detached

A decline in new listings in April likely contributed to slower sales compared to last month. However, sales are still relatively strong and on a year-to-date basis and remain nearly 30 per cent higher than last year and nearly double the long-term average. As the slower pace of sales was met with a decline in new listings, there was little change in the inventory situation and this segment continues to favour the seller.

Tight market conditions caused further price gains in the semi-detached sector. In April, the benchmark price reached $487,900, nearly two per cent higher than last month and over 16 per cent higher than last April.

Tight market conditions caused further price gains in the semi-detached sector. In April, the benchmark price reached $487,900, nearly two per cent higher than last month and over 16 per cent higher than last April.

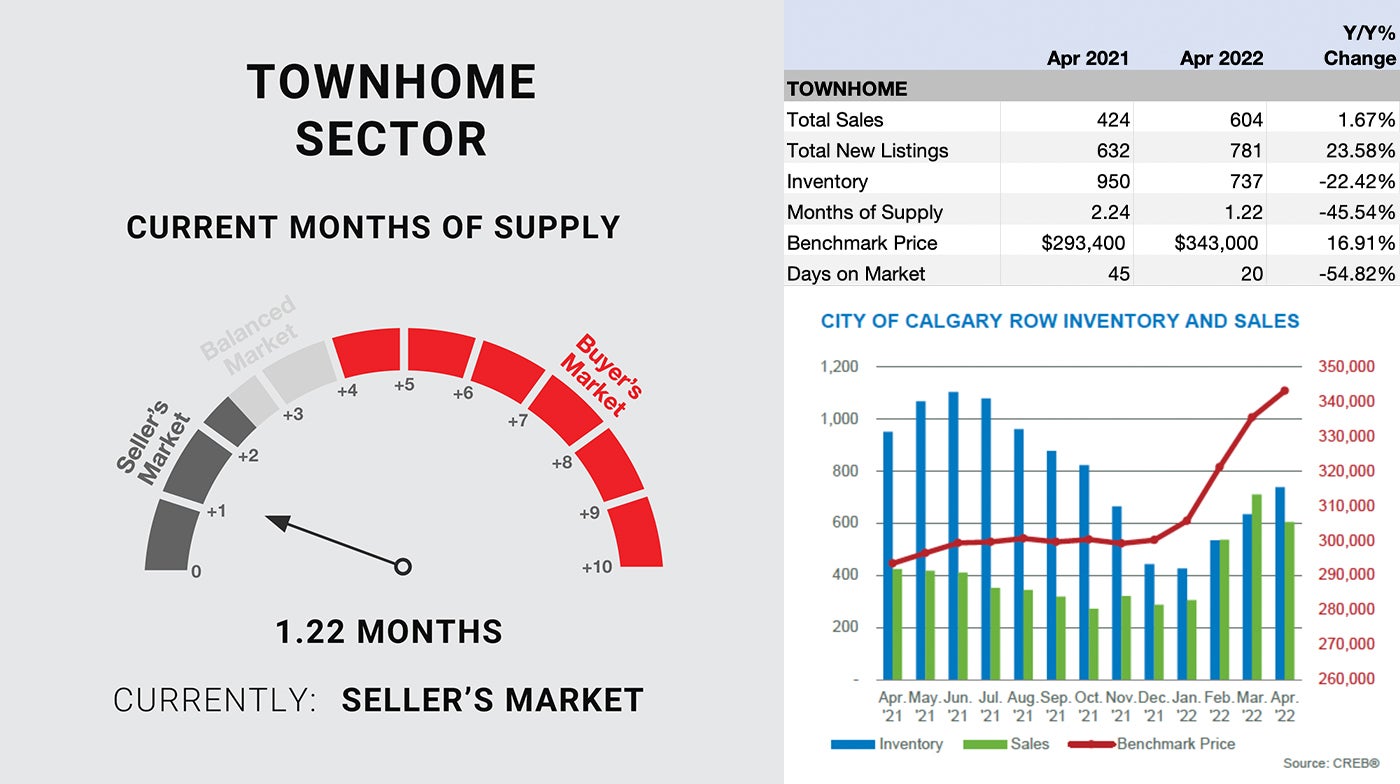

Row

While levels trended down from the previous month, new listings reached 781 units this month. This is a year-over-year gain of 24 per cent and the highest level ever seen in April. The improvements in new listings helped support stronger sales activity which rose over last year’s levels and set a new April high. This boost in new listings did cause inventories to trend up compared to earlier in the year, but it was not enough to pull the market out of the sellers’ market conditions.

With just over one months of supply, persistently tight market conditions continue to place upward pressure on prices. Thanks to gains across every district, row prices rose by over two per cent compared to last month and are nearly 17 per cent higher than last year.

With just over one months of supply, persistently tight market conditions continue to place upward pressure on prices. Thanks to gains across every district, row prices rose by over two per cent compared to last month and are nearly 17 per cent higher than last year.

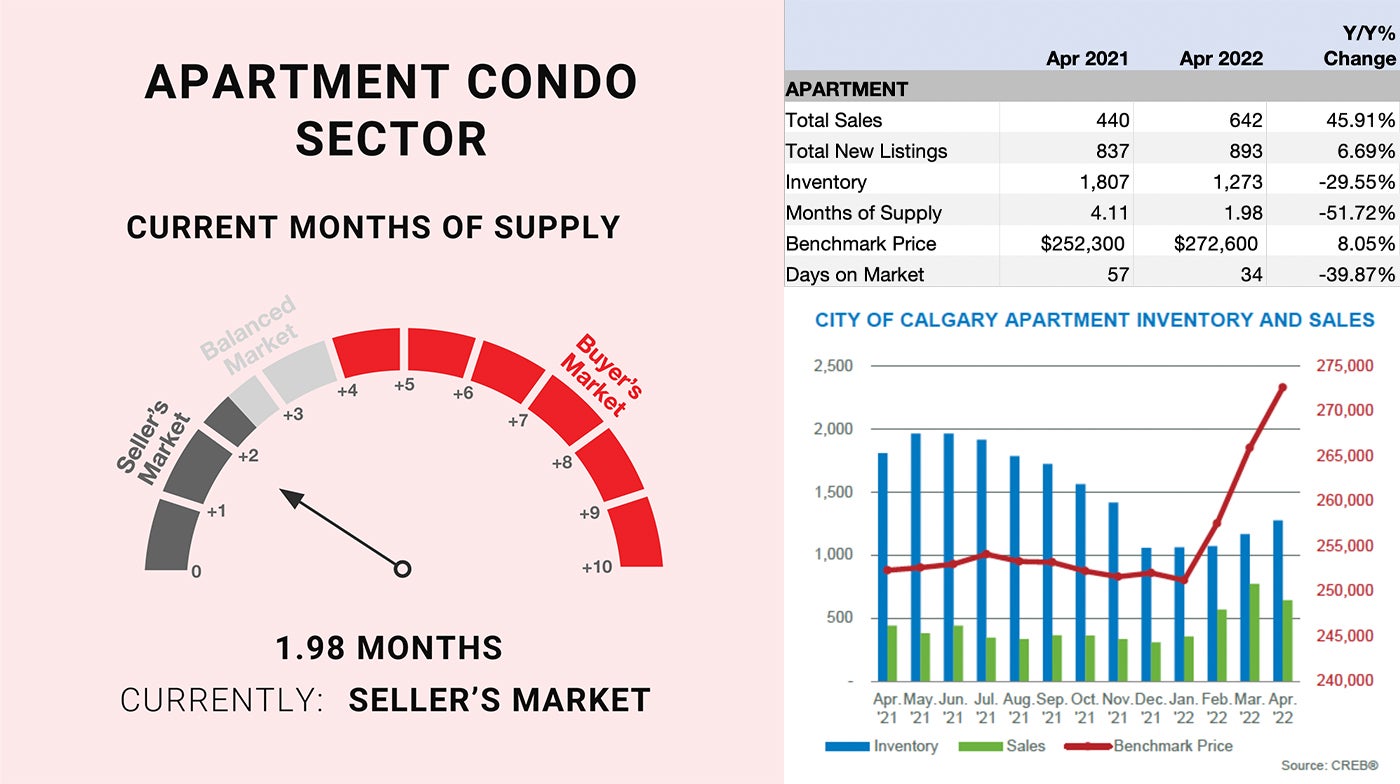

Apartment Condominium

Like other property types, apartment condominium sales did ease relative to last month’s record highs. But with 642 sales this month, activity still improved by over 46 per cent compared to last year reaching a record high for April. This in part was possible thanks to the 893 new listings that came onto the market. While it was not enough to dramatically change the supply levels in the market, the months of supply did edge up to nearly two months.

Tighter market conditions continued to cause prices to trend up in April. The apartment benchmark price rose across all districts and currently sits eight per cent higher than levels recorded at this time last year. The strong price gains over the past three months have helped narrow the spread from the 2014 record high price.

Tighter market conditions continued to cause prices to trend up in April. The apartment benchmark price rose across all districts and currently sits eight per cent higher than levels recorded at this time last year. The strong price gains over the past three months have helped narrow the spread from the 2014 record high price.